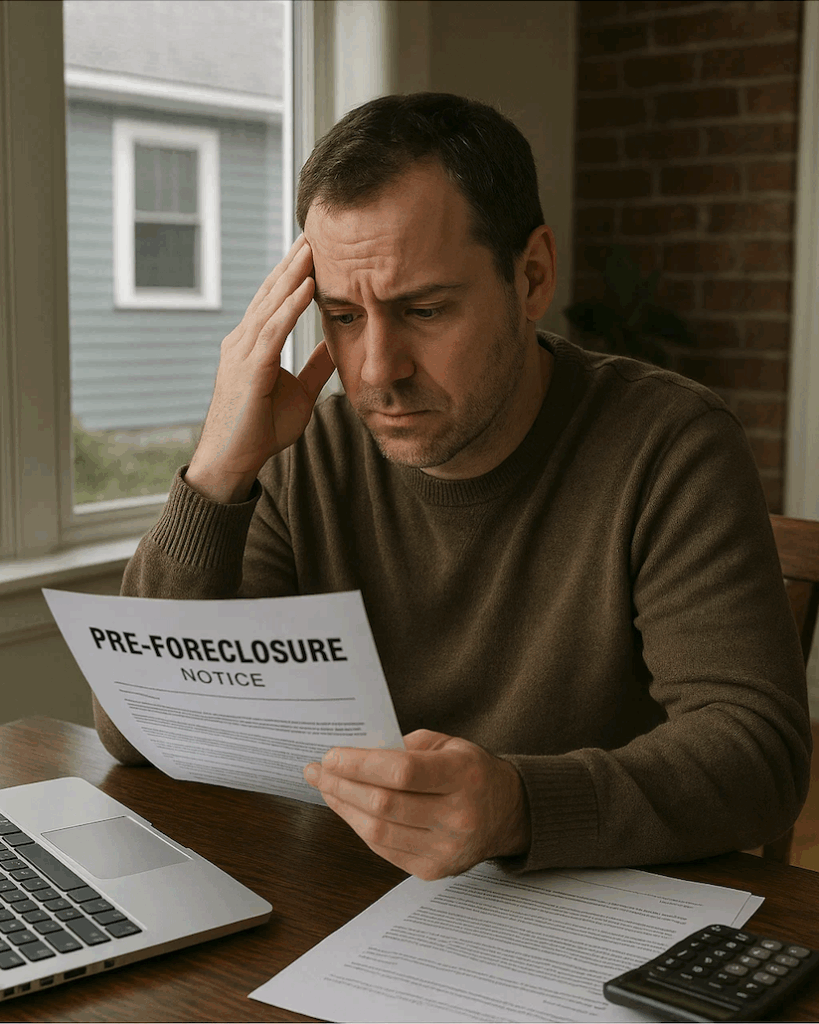

Few things are as stressful as falling behind on your mortgage. If you’ve missed several payments, you may receive a pre‑foreclosure notice — a formal warning that the lender may begin taking back the property. Pre‑foreclosure is not eviction; you still own the home and have a window to resolve the issue before the foreclosure process begins. Acting quickly during this stage can often prevent a full foreclosure and the lasting damage it brings .

This guide explains what pre‑foreclosure means, the options available to homeowners, and the consequences of waiting too long. We’ll finish by discussing a fast, hassle‑free option: selling your house to a cash buyer before the foreclosure process proceeds.

What Is Pre‑Foreclosure?

Pre‑foreclosure is the period between mortgage delinquency and formal foreclosure. When you fall behind on payments — usually 45–60 days for many lenders , though some states allow up to three missed payments or about 120 days — your mortgage servicer may file a Notice of Default (NOD). This document signals that you’re in default but still legally own the property. Lenders are required in many states to contact the borrower before filing the NOD (in California, at least 30 days’ notice is required). During pre‑foreclosure you retain legal title and have time to resolve the issue.

Steps to Stop Foreclosure

1. Pay the Past‑Due Balance

The most direct way to resolve pre‑foreclosure is to bring your loan current. Many lenders will halt foreclosure proceedings if you pay the arrears, either with a lump sum or through a repayment plan that spreads the overdue amount across future payments. Repayment plans help homeowners catch up by adding part of the missed payments to upcoming bills. If you can mobilize funds — perhaps from savings, a retirement account or family assistance — this option avoids negative credit events and preserves your equity.

2. Negotiate With Your Lender

Lenders would rather avoid the cost and complexity of foreclosure . Contact your mortgage servicer as soon as you anticipate trouble; they may offer several remedies :

- Loan modification: Permanently alters the loan’s terms (e.g., interest rate or length) to reduce the payment.

- Forbearance: Temporarily suspends or reduces payments during hardship.

- Repayment plan: Adds missed payments to future instalments.

Early communication is critical; lenders are more likely to work with borrowers who act before the situation worsens.

3. Sell Your Property

If catching up on payments isn’t feasible, selling the home can prevent foreclosure. A sale may satisfy the debt entirely or, if the home’s value is lower than the loan balance, a short sale may be negotiated with the lender. Selling during pre‑foreclosure gives you more control and can be less damaging than a foreclosure. According to Investopedia, selling in pre‑foreclosure can protect your credit while allowing the lender to avoid legal costs .

4. Deed in Lieu of Foreclosure

A deed in lieu allows you to transfer ownership of the property back to the lender. This voluntary action can simplify the outcome and may include negotiated relocation assistance or forgiveness of any remaining balance. Not all lenders accept this option, especially if other liens exist, but it can be a graceful exit when a sale is not possible.

5. File for Bankruptcy (Last Resort)

Bankruptcy (often under Chapter 13) can temporarily stop foreclosure and allow you time to reorganize debt. However, bankruptcy is complex, can harm your credit, and should only be considered with legal advice.

6. Seek Professional Advice and Housing Assistance

Government programs and non‑profit housing counselors can help you explore options. USAGov recommends contacting your lender immediately and not waiting until you’re unable to pay . It also cautions against scams that charge upfront fees for “foreclosure relief” . HUD‑approved counselors and state programs like the Homeowner Assistance Fund offer free guidance and, in some cases, financial aid .

CONSEQUENCES OF DOING NOTHING.

Failing to act during pre‑foreclosure can lead to serious consequences:

- Credit damage: Pre‑foreclosure itself may not severely hurt your credit, but a completed foreclosure can significantly lower your score . Foreclosure remains on your credit report for up to seven years and can impede future borrowing.

- Deficiency judgments: In some states, lenders may pursue the remaining loan balance if the sale doesn’t cover your debt .

- Eviction and loss of equity: Once foreclosure proceedings finish, you may be evicted and lose any equity in the home. Banks often sell foreclosed properties at a discount to recover costs .

- Long‑term financial stress: Foreclosure can make it difficult to rent or buy another property and may affect employment opportunities that review credit history.

In short, inaction leads to foreclosure. The earlier you take steps, the more options you retain and the less damage you incur.

A Quick Sale to Avoid Foreclosure: Why Sell to a Cash Buyer?

If catching up on payments or negotiating with the lender isn’t viable, selling your home quickly can be the best way to avoid foreclosure. Here’s why a cash sale is attractive for homeowners in distress:

- Speed: Traditional listings and bank approvals can drag on for months. A direct cash offer closes faster — often within days — allowing you to stop the foreclosure process and move on.

- Certainty: Cash buyers aren’t reliant on mortgage approvals, reducing the risk of a deal falling through. Once you accept the offer, you know exactly when your mortgage will be paid off.

- No repairs needed: Cash buyers typically purchase homes “as is,” sparing you from costly repairs or inspections when you’re already strapped for cash.

- Credit protection: By avoiding foreclosure, you protect your credit from the most severe damage , making it easier to qualify for future loans or rentals.

Our real‑estate team specializes in helping homeowners facing pre‑foreclosure. We understand the urgency of your situation and can make a fair, no‑obligation cash offer for your property. You get to sidestep the legal and emotional toll of foreclosure, preserve your credit as much as possible, and move forward with peace of mind.

Get An Offer Today – Sell In A Matter Of Days

Receive a fair cash offer with no obligations. No agents. No fees.

Final Thoughts

Pre‑foreclosure is a warning, not a sentence. Although receiving a notice of default is frightening, you still have control. By contacting your lender early, exploring loan modifications or forbearance, and understanding options like repayment plans, short sales, or a deed in lieu, you can often keep your home or exit gracefully. Acting quickly is critical — every missed month narrows your options and increases the likelihood of foreclosure. And if other solutions aren’t feasible, selling to a cash buyer offers a fast, reliable way to resolve your mortgage, protect your credit and move forward.

Ready to explore your options? Reach out today for a confidential conversation and get the guidance you need to stop pre‑foreclosure in its tracks.

Disclaimer: This article is for informational purposes only and should not be considered legal or financial advice. Homeowners facing foreclosure should consult with a qualified attorney, housing counselor, or financial advisor for guidance on their specific situation.